In this blog post, John Murphy, Director/Partner of OmniPro Tax and Legal Limited, Chartered Accountant and a Chartered Tax Adviser with almost 20 years of experience in the industry will take us through a real-life case that highlights the importance of staying up-to-date with tax laws and regulations in relation to the sale and purchase of a Company/business. We have the expertise and experience to guide you through every step of the process. We pride ourselves on being able to not only provide tax and company law advice on the restructuring/sale/purchase but also being able to implement any restructuring plan as we provide company secretarial, corporate finance, business valuation and company law services as part of our offering.

Background Facts

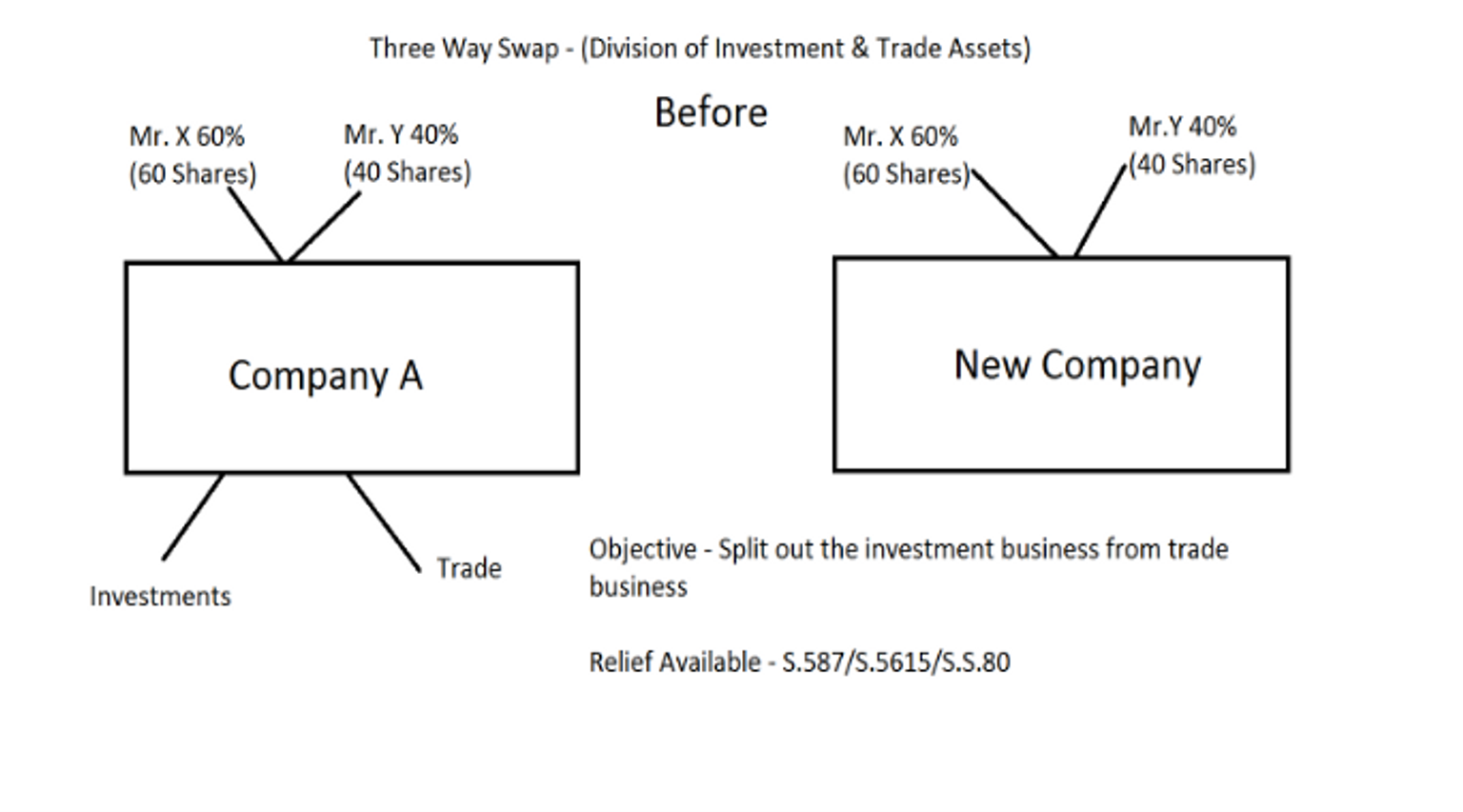

- Company A – holds investments & trade assets

- Potential purchaser not interested in investments

- Purchaser would like to purchase assets, but Seller wants to sell shares

- Pre-sale restructuring to affect a share sale (subject to revenue pre-approval & no heads of agreement/letter of intent obtained)

- Example illustrates where investments & trade exists. Applicable if only one trade & potential purchaser where potential purchaser would not want certain assets/debts

- Purchaser has agreed to purchase shares for €1 m upfront and if profits increase to €110k within 2 years an additional €400k or if maintain current trends €200k

- Subsequently New Co. is purchased

- Mr X held the shares for 4 years/Mr Y 10yrs & worked in managerial & technical capacity

- Shares received by Mr X as gift from parents 4 years ago:

- Retirement relief claimed by parents (tax saved of €70k)

- Business asset relief claimed by Mr X at that time (tax saved of €4k) – Base cost for Mr X of €40k.

Advise to Sellers:

Pre-sale restructuring carried out - Steps Taken Prior to the Sale

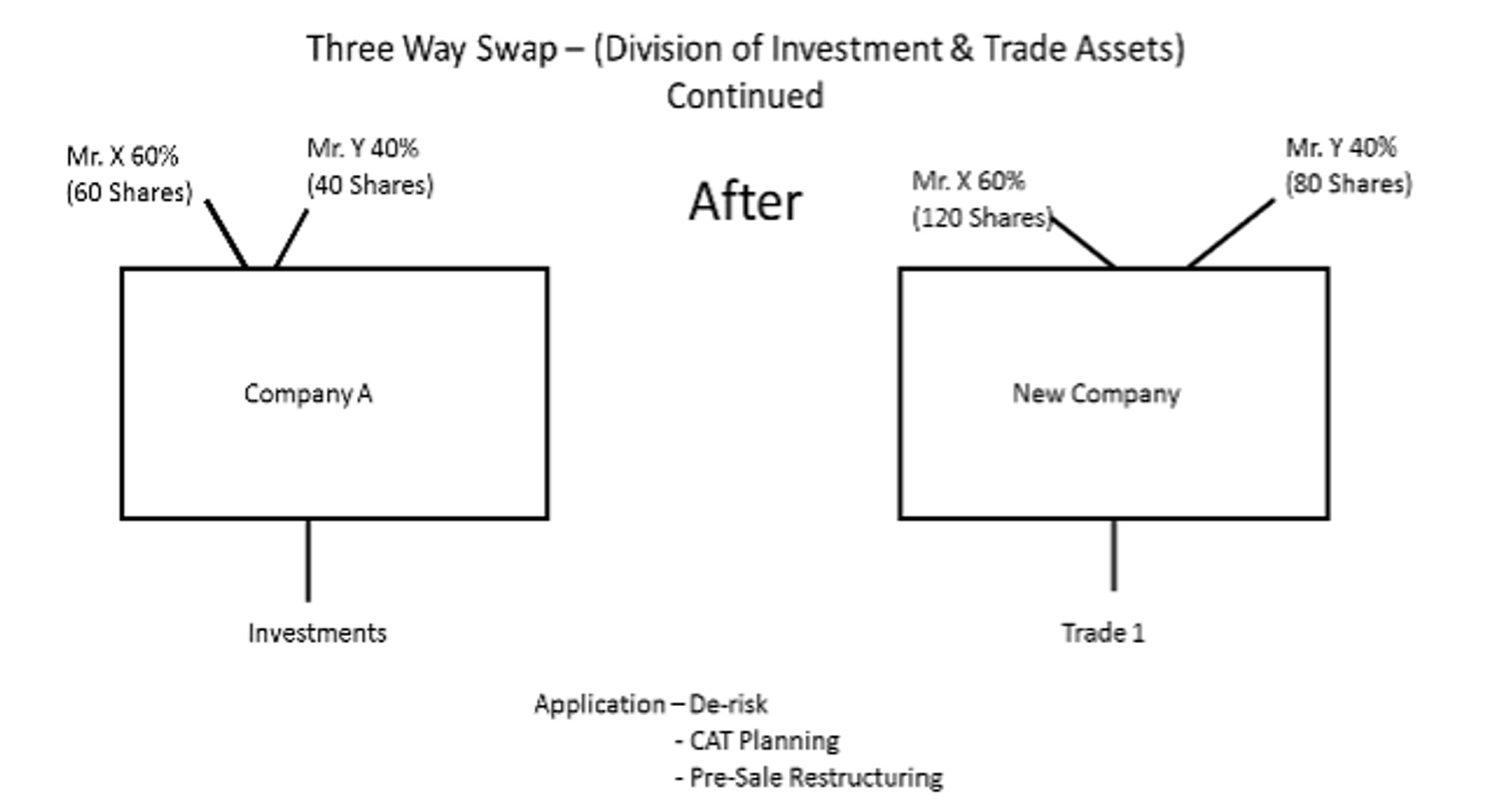

In this case, we advised to transfer out the trade from Company A to a New Co. incorporated just before the transfer (which was owned in the same proportions by the same persons as New Co.) in return for shares being issued to the shareholders of Company A in the same proportions as each held in Company A. There are various reliefs to ensure that this transfer can be carried out at no tax cost once it is structured and implemented correctly. The transfer to the New Company does not affect the period of ownership and directorship/employee-ship for the various reliefs. This step was taken as firstly the Sellers did not want to dispose of the investment assets, secondly, the purchasers were not interested in them, thirdly it resulted in no dilution of retirement relief and potentially entrepreneurial relief and fourthly, it reduced Section 135(3A) TCA risks (as discussed below). The before and after result has been illustrated below:

Other actions taken as part of this step:

- SAP 204 (Summary approval procedure) carried out to permit the transfer as sufficient reserves did not exist to permit the transfer of assets out.

- Company A swaps names with New Company

- Stock transfers under S.89 TCA

- No balancing allowance/charge under S.400

- Part of the due diligence identified a risk of S.80 SDCA so indemnity put in place to cover this (albeit reluctantly).

- Ex-gratia payment made on retirement

Tax for sellers

The first step is to assess whether Section 135(3A) can be invoked here to tax the proceeds as a dividend subject to income tax.

As a result of the change made by Section 22 of Finance Act 2017 which is effective 2 November 2017, there is a potential risk that this might come within the remit of the new Section 135(3A) as indirectly New Co. will provide funds to allow Purchase Co. to pay for its shares by way of dividends (whether paid before or after the purchase). As Section 135 is currently drafted this would be caught and therefore Mr X & Mr Y would be deemed to have received a dividend and therefore the relevant element of the proceeds liable to income tax as opposed to CGT. Under the wording in Section 135(3A) TCA this dividend is from assets being used of the Purchase Co. to fund the purchase of the shares by New Company from Mr X & Mr Y. However, Revenue has stated in Tax and Duty Manual Part 06.02.05 that bonafide transactions do not come within the remit by concession where the initial upfront payment is paid from bank debt or other personal resources. On the basis that this is a bonafide transaction, and the seller is not mandating how the purchase money (contingent consideration) is to be funded and are not party to this, then Section 135(3A) should not apply. Note however, a revenue concession is not in the legislation so therefore the advisor would advise the seller that if the revenue wanted to go to the Appeal Commissioner the Appeal Commissioner can only look at the legislation so technically, they would likely find that it did come within the remit of Section 135(3A) TCA. The basis for non-application of Section 135(3A) in this case is as follows:

- The consideration for the disposal is based on a commercial valuation and this valuation has been determined based on an arm’s length transaction between two unconnected parties

- The company being sold does not have excess cash and is held for trading purposes only

- The payment arrangements appear to be in line with acceptable industry norms

- The initial payment is being financed from the acquiring company’s own resources (i.e. by bank financing or by way of a director’s loan).

- It is evident that the future cash flows show that the deferred element will be covered from future cash flows of the business such that it is evident that any payments in the future will be from future profits as opposed to using the net assets in existence at the time of the purchase

- Earn-out – as ascertainable = CGT payable on full amount upfront i.e. €1.4m (split by X &Y)

- If turns out that less than €400k was received – revenue will issue a refund.

- No CG50-shares not deriving value from land etc.

- Lump sum ex-gratia (assuming not in employment contract) can be paid tax free up to SCSB or increased exemption whichever is higher. – would be discussed with purchaser

Tax for seller – Mr X

- Assume base cost of €40k base cost split under S.584(6) between Co. A & new Co.):

- CGT payable on current disposal

- N/a Retirement relief (“RR”) as not owned for 10 yrs

- Entrepreneurial relief applies

- First 1m of chargeable gain at 10% - 800k (€840k – base cost €40k) utilised for this sale.

- Clawback of RR of €70k payable at time of sale as disposed of within 6 yrs – S.598;

- Clawback of business asset relef (“BAR”) claimed as disposed of within 6 yrs.

- CGT/CAT credit (S.104 CATCA) utilised to result in nil CAT tax as CGT paid exceeded CAT that would have been payable (as not disposed of within 2 years).

- No VAT to be charged on sale of shares.

- No VAT deduction for professional fees

Tax for seller – Mr Y

- No VAT on sale of shares

- Assume base cost of nil when split under S.584(6) between Co. A & new Co.):

- CGT payable on current disposal

- Retirement relief applies = Nil CGT (as proceeds of 560k under €750k and owned for 10 yrs etc.)

- CGT payable on current disposal

- Entrepreneurial relief N/A as higher tax than RR = 56k (560k*10%)

- FYI First 1m at 10% = 560k (€560k – base cost €nilk) utilised for this sale.

Structure for purchaser (while not concerned in this real life example – we have illustrated this for completeness)

- Purchases incorporated New Company ‘Purchase Co.’

- ‘Purchase Co.’ purchases shares – part from equity introduced, loan from directors of Purchase Co. and part from bank borrowings;

- ‘Purchase Co.’ get S.247 interest deduction which is utilised to reduce tax of group (i.e. ‘Purchase Co.’ & ‘New Company’)

- Loan in ‘Purchase Co.’ repaid from dividends received from ‘New Company’ – elect to ignore for close Co. Surcharge (S.434A TCA). Seller is not party to this arrangement, nor do they know how the part loan will be repaid.

NB - Note as a result of the change made by Section 22 of Finance Act 2017 which is effective 2 November 2017, there is a potential risk that this might come within the remit of the new Section 135(3A) as indirectly New Co. will provide funds to allow Purchase Co. to pay for the shares by way of dividends (whether paid before or after the purchase). As Section 135 is currently drafted this would be caught and therefore Mr X & Mr Y would be deemed to have received a dividend and therefore the relevant element of the proceeds liable to income tax as opposed to CGT. Under the wording in Section 135(3A) TCA this dividend is from assets being used of the Purchase Co. to fund the purchase of the shares by New Company from Mr X & Mr Y. However, Revenue have stated in Tax and Duty Manual Part 06.02.05 that bonafide transactions do not come within the remit by concession where the initial upfront payment is paid from bank debt or other personal resources. On the basis that this is a bonafide transaction, and the seller is not mandating how the purchase money (contingent consideration) is to be funded and are not party to this, then Section 135(3A) should not apply. Note however, a revenue concession is not in the legislation so therefore the advisor would advise the seller that if the revenue wanted to go to the Appeal Commissioner the Appeal Commissioner can only look at the legislation so technically, they would likely find that it did come within the remit of Section 135(3A) TCA.

Tax for purchaser

- VAT on professional fees – possible if Purchase Co. is carrying out an economic service for the subsidiary (e.g. provision of management services to New Company).

- No CG50-shares not deriving value from land etc.

- Stamp duty at 1% of €1.4m= €14,000

At OmniPro, we understand that buying or selling a business can be a complex and challenging process, and we are here to help accountants and their clients. We have the expertise and experience to guide you through every step of the process. We pride ourselves on being able to not only provide tax and company law advice on the restructuring/sale/purchase but also being able to implement any restructuring plan as we provide company secretarial, corporate finance and company law services as part of our offering.

If you require assistance with selling or purchasing a business or sourcing a purchaser for your clients, please contact John on 053 91 000 00 or email [email protected].