Chapter 13 of the Companies Act 2014 sets out the obligations in relation to filing a Company's annual return and the documents annexed to it. It is the obligation of the company officers (Directors and Secretary) to ensure that the annual return is filed on time with the Companies Registration Office.

What is an annual return?

The annual return is a document that sets out certain prescribed information which is required to be delivered to the Companies Registration Office (CRO) by any Irish company, whether it is trading or not, at least once every year. This annual return form must be delivered to the CRO by electronic means using CRO’s CORE platform or a secretarial software package. The filing fee of €20 must also be paid online. The use of manual B1 forms is no longer permitted.

Who must file an annual return?

The annual return form must be filed by every company incorporated in Ireland, this return is due even if your company is not trading.

Failure to submit your annual return will result in your company incurring substantial late filing penalties and the loss of audit exemption for the following two years under the Statutory Audit Act 2018 and may be struck off the Register.

When must my annual return be filed?

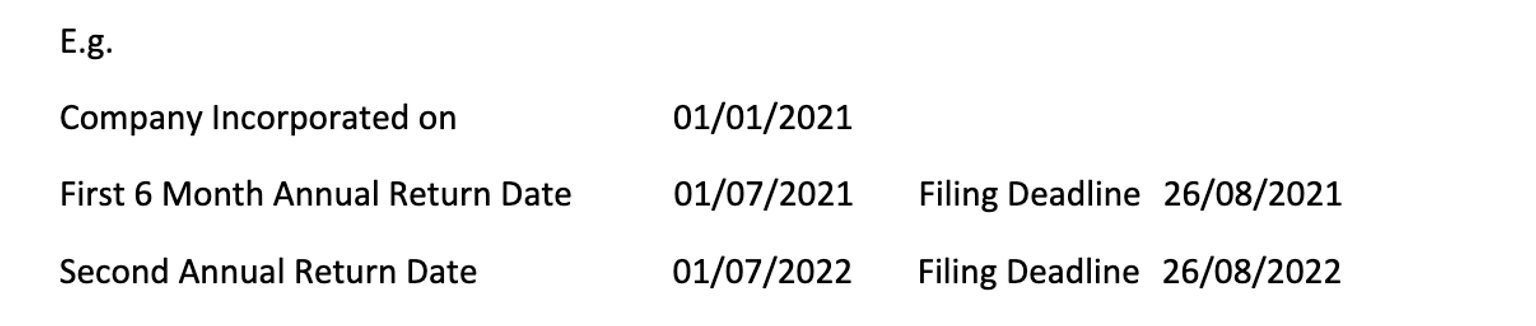

The first annual return of the company is due to be filed 6 months after the company is incorporated. Financial Statements are not required to be uploaded with this return. The annual return is then due annually from this date.

The annual return form together with the financial statements (and any other required documents) must be filed and uploaded to the CRO within 56 days of the company's annual return date.

Payment must also be made by this date for the annual return to be regarded as filed on time.

Commons Errors when filing the Annual Return Form B1

- Entering the incorrect email address for the company, this should be the presenter or a known active email address of the company as correspondence from the CRO may be sent to here.

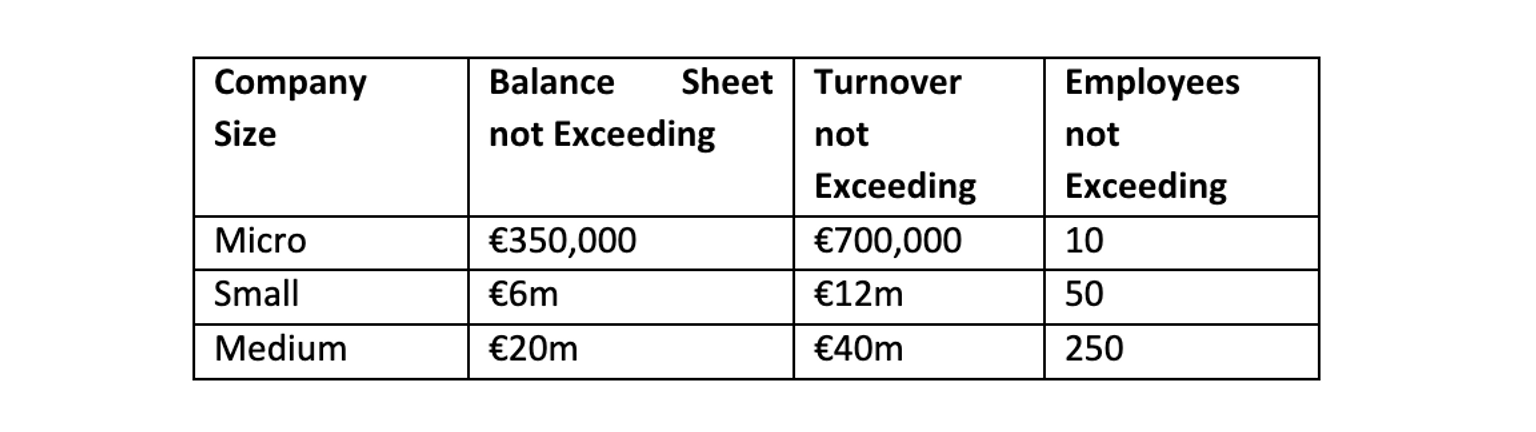

- Presenters being unsure of the company size, this information can be ascertained from reading the accounts and determining which category the company falls into the company sizes are set out below:

- Inserting the incorrect financial year.

Under Section 288 of CA 2014 the financial statements attached to the company’s first full annual return the financial period must be from the date of incorporation and the maximum length can be 18 months.

Each subsequent financial year must start on the day immediately following the previous period's end and must be 12 months + or – 7 days in length.

The + or – 7 days can cause issues in a leap year where you will need to change the accounts year-end and the period on the B1 to 29th Feb.

If the financial year is not the same as on the accounts that are submitted the CRO will return the B1 to you to be amended and refiled within 14 days.

- The Accounts will not upload.

The Financial Statements must be uploaded as a single document in PDF format, other formats will not be accepted and they must be less than 5 MB in size.

- Non-EEA Resident Director

An error we encounter on the B1 form is the Directors' residency defaulting to being Non-EEA resident and you must tick to change this for each Director (if applicable). CORE will not allow a B1 to be filed unless at least one of the Directors is selected as being an EEA resident or the company has a section 137 Bond in place.

- Not completing the filing in time.

Another common pitfall of the new filing system is agents not allowing themselves sufficient time to arrange for the director and secretary to sign the B1. Financial Statements are now required to be uploaded before the B1 signature page can be generated, what we see frequently happening is accountants using the 56 days past the ARD as the time to complete their accounts, this in turn gives the filing agent less days to complete the B1 and arrange for the B1 to be signed by the Director and Secretary.

- Not Completing the Payment

A common mistake that happened when the new CORE platform launched was filing agents uploading the annual return signature page and not completing the filing by making the payment. If you do not complete the payment stage of the annual return before the 56-day deadline the B1 will be deemed to be late.

During the peak filing period for companies in Ireland (there are over 52,000 companies with 30th September ARD’s and these have a final filing deadline of 25th November). We advise all filing agents to file their annual returns well in advance of this 25th Nov deadline. In previous years the CRO’s systems have not been capable of dealing with the filing of such a large volume of returns on one date and the system may experience disruptions. This can cause delays in obtaining the signature page or completing the submission.

What’s changing in 2023?

Section 35 of The Companies Corporate Enforcement Act (2021) which has not yet been enacted will require directors to file their Personal Public Service Numbers (PPSNs) with the CRO when incorporating when filing the company's annual return, updating their details, being appointed as a Director or incorporating a new company.

While no exact implementation date has been confirmed it is estimated that this will be in the second quarter of 2023 and the information will be required on the company's next filing and all future filings. There is no indication currently of the process for non-resident or non-tax registered directors.

The PPSN and transaction numbers will not be visible on the annual return form and this is for verification purposes only

Companies and their directors should now ensure that they know their PPSN and the variation of their name registered with the DEASP, as they will not be able to file their annual returns without this information. Any delays in confirming these details could risk the company's annual return being late and the company will then be subject to late filing fees and loss of audit exemption for the next two years.

Please note this information is accurate based as of today’s publication and may be subject to change.

If you require assistance or advice in relation to any of the above matters, please contact our team on 053 91 000 00 or email [email protected].