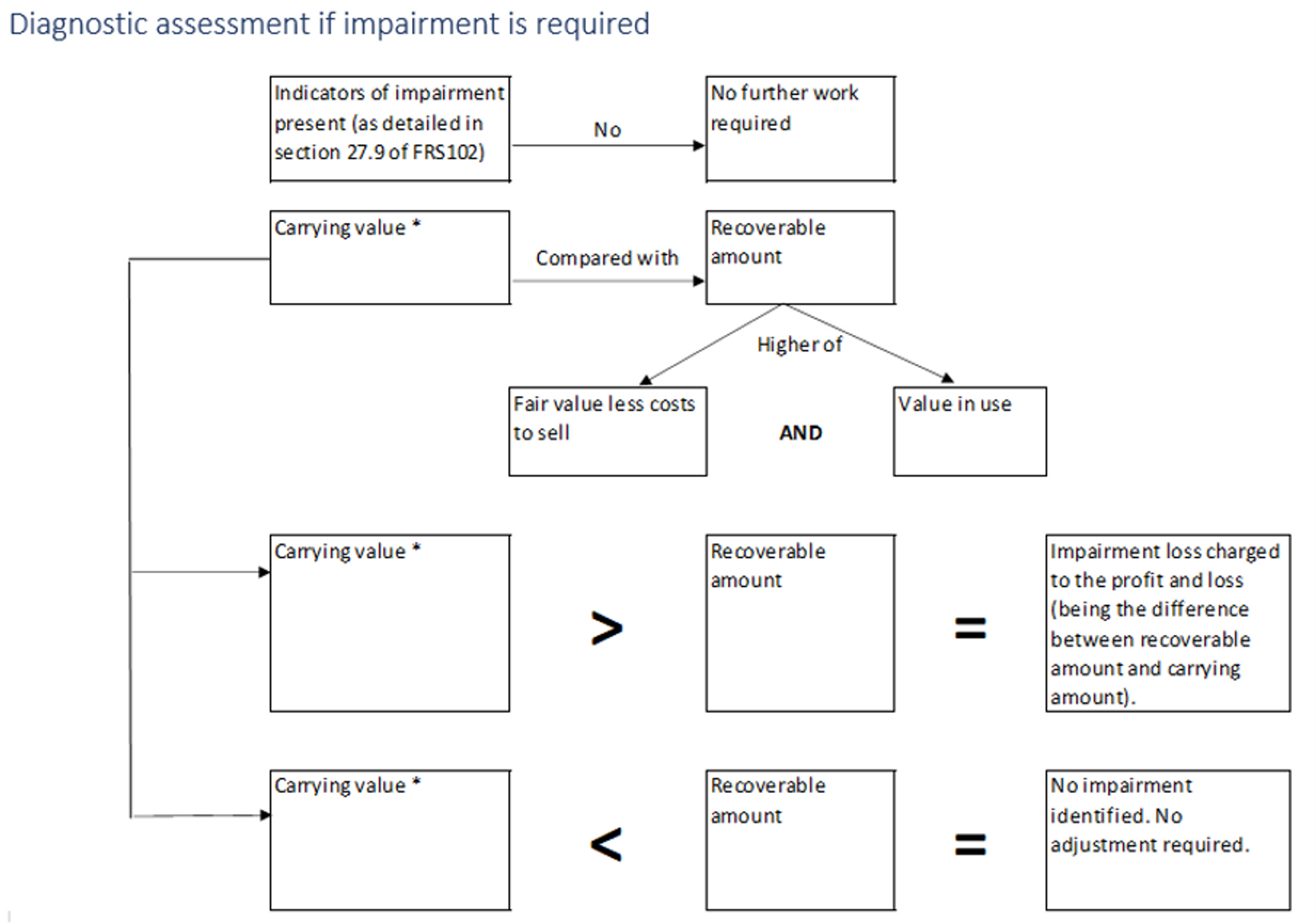

The directors of a company are required to assess, at each balance sheet date, whether there are any indicators that an asset, or collection of assets, may be impaired. If such an indication exists, then the directors must estimate the recoverable amount of the asset [FRS 102 27.7].

The past number of years has given rise to multiple challenges for companies – the global pandemic, the impact of Brexit, ever-rising inflation and costs, and so on. It is likely that many companies will be in a position of needing to do an impairment review on their fixed assets at the end of the financial year.

When assessing whether an actual impairment charge is required, the directors of an entity are required to establish the recoverable amount of the asset. This recoverable amount is defined to be the higher of the asset’s fair value less costs to sell and its value in use. Whether either of these values is higher than the current carrying value in the company’s financial statements, then no impairment is required. Where both values are lower than the current carrying value, then an impairment is required and should be posted as an expense through the profit and loss account.

Appendix 1 to FRS 102 includes the following definitions:

- Recoverable amount – the higher of an asset’s (or cash-generating unit’s) fair value less costs to sell and its value in use;

- Fair value less costs to sell – the amount obtainable from the sale of an asset or cash-generating unit in an arm’s length transaction between knowledgeable, willing parties, less the costs of disposal;

- Value in use – the present value of the future cash flows expected to be derived from an asset or cash-generating unit.

Below is a flowchart that illustrates the process.

*Note: the carrying value can be the value of the individual assets where cash flows can be identified from the asset, or it can be a carrying value of a cash-generating unit where cash flows cannot be identified as specific to an asset. The starting point is an individual asset, then one should move to a CGU, or cash-generating unit. As can be seen from the above, it may not always be necessary to calculate the fair value less costs to sell and the value in use: if one of the measures gives a value which is greater than the carrying value this indicates no impairment is required so there is no need for further work to be performed to assess the other measure.

Question:

Entity A provides tourist helicopter flights over Dublin city. Management is reviewing all its assets for impairment as a result of the drop in sales following the pandemic.

One of A’s helicopters is 2 years old, has a carrying value of €2.5m, and a value in use of €2.2m.

The market for these assets is an active one, and there are often sales and purchases made of similar assets internationally. A similar asset was recently sold to a US conglomerate for €2.6m. The estimated incremental costs that would be directly attributable to the disposal would be €40,000.

Management has no intention of selling the helicopter if it can help it. They are proposing to recognise an impairment based on the value in use being €300k below the carrying value.

Answer:

In summary:

Value in use = €2.2m

Fair value less costs to sell = €2.6m - €40k = €2.56m

Recoverable value (higher of the above two figures) = €2.56m

Net book value/carrying value = €2.5m

Management’s conclusion is not correct. This is because the recoverable amount (being the higher of value in use and fair value less costs to sell) still exceeds the carrying amount.

Management could recover the asset’s carrying value if it chose to sell it rather than use it in its operations; as a result, no impairment is required in this situation.