Posting impairment charges

When management has established the recoverable value of an asset, or a group of assets, and it is lower than the current carrying value in the financial statements, the difference between the two values must be posted to the profit and loss account as an impairment charge.

Impairments are calculated on an individual asset basis. Where it is not possible to estimate the recoverable value of an individual asset, the smallest cash-generating unit, or CGU, to which the asset belongs is used [FRS 102 27.8].

When posting an impairment charge to a CGU, certain steps must be followed. The impairment charge must first be used to reduce the carrying amount of any goodwill allocated to the CGU, and only after that allocation can the remainder of the impairment charge, if any, be allocated to the remaining assets, on a pro-rated basis [FRS 102 27.21].

An example of this allocation is given below:

Question:

In 20X1, Parent A acquired Company X for €100,000.

On acquisition, 3 separate cash-generating units were identified; these are called CGU1, CGU2 and CGU3.

The fair value of assets acquired was €70,000, and goodwill of €30,000 was recognised and set against each CGU. The goodwill was allocated to each CGU based on the synergies expected to be achieved, which ultimately was 1/3 to each CGU.

In 20X2, due to a change in market trends, the demand for the product produced by CGU1 reduced significantly. The value in use calculations indicates a recoverable amount of €9,000 for that CGU. The fair value less costs to sell was calculated as being €7,000.

The current carrying values of the assets are:

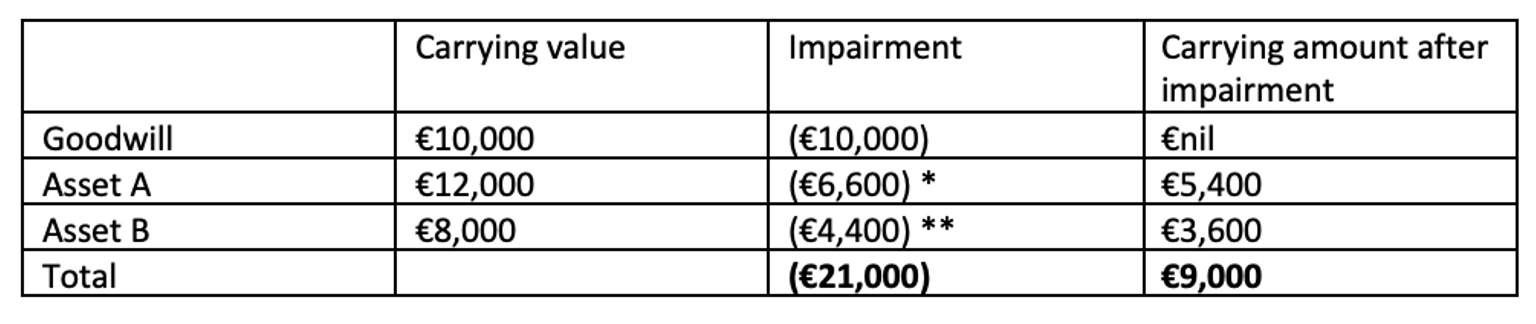

Goodwill = €10k

Asset A = €12k

Asset B = €8k

Answer:

The recoverable amount is defined as being the higher of the fair value less costs to sell and the value in use. In this instance, the higher figure is the value in use of €9,000. As the current carrying value of this group of assets is €30k, a total impairment is required of €21k.

When dealing with CGUs, the impairment must fully be allocated to goodwill, and then any remaining impairment split between the remaining assets.

Therefore, €10k of the €21k impairment will be automatically allocated to goodwill. The remaining €11k will be split between assets A and B pro rata:

* impairment allocated pro-rata to identifiable assets e.g. asset A= €11,000 * (€12,000/ (€12,000+€8,000)) = €6,600.

** impairment allocated pro-rata to identifiable assets e.g. asset A= €11,000 * (€8,000/ (€12,000+€8,000)) = €4,400.